BLOG: Buying Your First Home (in England) – A Simple Guide!

Posted February 3, 2026

Buying your first home can feel overwhelming — especially when you’re faced with jargon, percentages, and confusing numbers.

So instead of throwing all that at you, here’s a simple, real-life example to show how the process actually works.

Meet Sarah

Sarah is 29, earns £38,000 a year, and has £22,000 saved. She’s a first-time buyer and wants to purchase her first home — but isn’t sure where to start.

What Is a Mortgage?

A mortgage is a loan from a bank or building society that helps you buy a property. You repay it monthly, with interest, over a long period — typically 25 to 40 years. Most lenders allow mortgages to run until age 70–75.

Sarah’s Example:

Property price: £220,000

Deposit: £20,000

Mortgage: £200,000

Loan-to-value (LTV)*: 90%

*Loan to value (LTV) – compares the mortgage amount you borrow to the property’s value, expressed as a percentage. Lenders use “LTV” to assess risk; a lower LTV (meaning a bigger deposit) signifies less risk, often leading to better interest rates and cheaper monthly payments, while a higher LTV (smaller deposit) is riskier and typically results in higher rates.

Deposit & Affordability

Before Sarah starts viewing properties, she speaks to me.

As an independent mortgage adviser, I can access the whole of the market — meaning I’m not tied to one lender or product.

We look at:

• Her income

• Her monthly budget

• Her credit history

This helps her understand:

• How much she can realistically borrow

• What monthly payments feel comfortable

• What type of property fits her budget

This step is key — it prevents wasted time and disappointment later on.

Mortgage Rates

Sarah chooses a fixed-rate mortgage, meaning her monthly payments stay the same for a set period. For many first-time buyers, this provides peace of mind — knowing exactly what’s leaving their bank account each month.

Other options, such as tracker mortgages, are available. These move up and down with interest rates, which can be cheaper at times but come with more uncertainty.

Stamp Duty – First-Time Buyers in England

First-time buyers in England pay no Stamp Duty on properties up to £300,000. Because Sarah buys her flat for £220,000, she pays nothing at all.

Rates correct as of the 20.01.2026 and are subject to change at any time.

Other Costs to Budget For

Your deposit isn’t the only money you’ll need. Sarah also budgets for:

• Solicitors’ fees

• Homebuyer survey (upgraded valuation)

• Mortgage arrangement fees

• Moving costs

• Buildings insurance

Being prepared for these costs avoids last-minute stress.

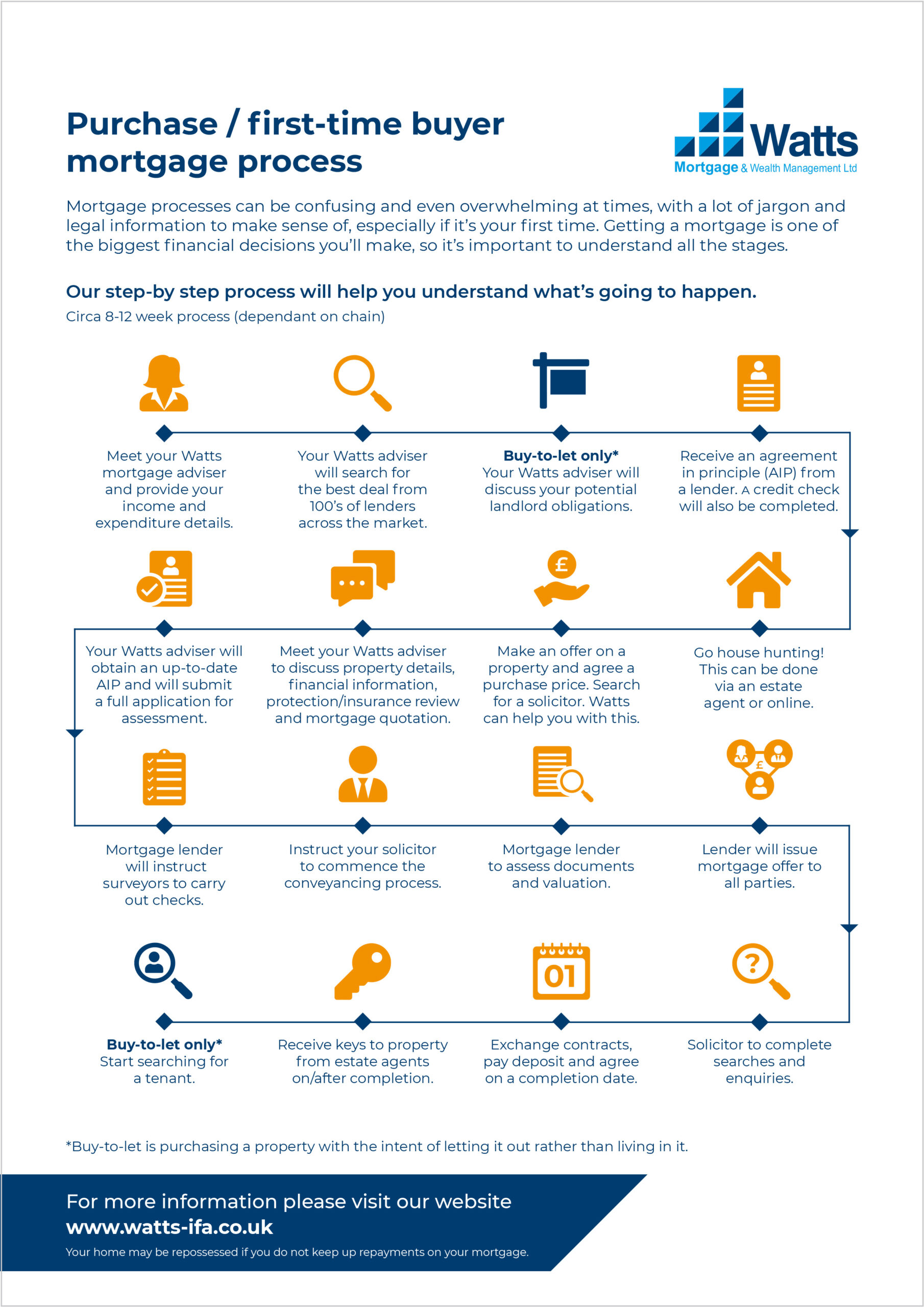

The Buying Process – Sarah’s Journey

My role is to guide Sarah through every step, including:

• Agreement in Principle

• Negotiating on properties

• Making an offer

Once her offer is accepted:

• I submit her mortgage application

• The survey is carried out

• The lender issues a mortgage offer

Solicitors handle the legal work, and once contracts are exchanged, everything becomes legally binding.

A few weeks later — completion day — Sarah gets the keys to her first home!

Buying your first home is a huge milestone. With the right guidance and clear information, it’s far more achievable than many people expect. If you’re a first-time buyer and don’t know where to start, Give Shannan a call on 01270 620 555.

View our first time buyers guide here.

{kind=link}